As small business owners, you contend with a host of issues on a daily basis. Over time, you develop resilience in handling the curve balls that are thrown your way. Then, after a good day’s work, even though you will likely say that it was moderately stressful, you have a sense of achievement and maybe a little bit of self-congratulation for the skills you have developed.

But there is one stress factor that does not work like this. It is that gut-wrenching, heart-stopping acknowledgment that you don’t have the funds to pay your bills or the wages.

Needless to say, most SMEs make mistakes when it comes to managing their cash flow. They tend to lack both discipline and processes to keep on track of their accounts payable.

While many don’t do any sales forecasting, of those that do, often they over forecasting sales, or don’t revise their forecast over time.

Business owners who are not able to efficiently manage their cash flow are almost always doomed to crash. Poor cash flow management is an endemic problem not just in New Zealand, in fact, a U.S bank study found that 82 percent of all SME’s failed due to poor cash flow management.

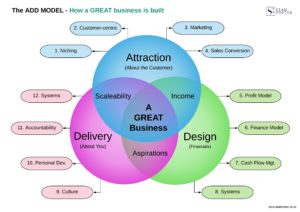

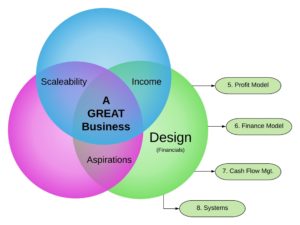

The ADD (Attraction-Design-Delivery) Model focuses on 12 key projects that make for a GREAT business.

One of these projects is Cash Flow Management. Managing the cash flow in your business is that important. It needs to be proactively managed.

Want to learn more about ADD?

Importance of cash flow

Cash flow is the life force of any business. It’s the means to buy supplies, pay salaries and make infrastructure investments. Owners who manage their cash flow properly are empowered to improve nearly all aspects of their Business.

Converting sales into cash as fast as possible while reducing overall production costs is the key. A well-documented case example of this is Dell computers. Dell forged ahead in terms of their market share as a result of their unique strategy (unique amongst their competitors at the time), which allowed them to collect the money for sold computers before they paid their suppliers for materials.

Extending the “time-use” of money will, of course, play in your favour, if you are also able to extend your payments to suppliers. This principle is a great strategy for long-term, sustained business growth, whether your company is small or large.

Although there is a multitude of options to improve your cash flow, the following three should be regarded as essential to implement.

1. Avoid Surprises

Anticipate future needs by keeping accurate, timely records and budgets. This is crucial to make sure you’re on top of your business’ financial standing.

Every business has a different risk profile to cash management, as does the variability in how far ahead cash must be forecast. For instance, do you need to consider next month’s payroll or to pay for stocks that you must pay for months in advance?

I recommend that for cash-sensitive businesses, you examine your cash situation daily and at least weekly, you revise your forecast for the next two weeks.

Taking a longer-term view on your cash requirements depends very much on your business. However, the norm is to review what are your longer-term requirements, IE., over the next two to three months or at least on a monthly basis.

If you have not set up a cash flow forecast before, an easy way to start would be to utilize your income statements together with your balance sheet. You will know when you have set up your forecast report correctly by asking this simple question: Does it alert you in advance of any shortfalls, giving you time to prepare?

Do you need assistance with your Cash Flow Forecast?

2. Build Connections in the financial community

The odds are low when it comes to enticing investors or borrowing cash for your business right when you absolutely need it. It’s better to build your connections with lenders ahead of time before you need their help. Last minute, urgent calls for funding just send the alarm bells off.

If you were a lender, then would you not feel more secure about lending money to a proactive customer as opposed to a reactive one? If you are seen as “last-minute” and reactive, then what other “surprises” have you not foreseen?

Generally, banks make secured loans on the following assets:

Accounts Receivables

Normally, this is established as a revolving line, based upon a percentage of total accounts receivables (AR). Typically, 60 to 80 percent that’s due within a 60 to 90-day period. AR financing is one of the most common corporate loans there is.

Image from fortiviti

AR varies so the balance due moves up and down as well. When AR and sales increase, the bank advances more cash on the line. However, when it decreases, you have to make a payment to bring the loan in line with the agreed upon AR-to-loan ratio.

To give reassurances to your lender, they need to see that you are excellent at managing your receivables.

Are your debtor days (the average number of days your customers take to pay you) realistic and consistent month after month?

Do you have signed contracts and terms and conditions in place?

Do you make use of PPSR’s?

Are your sales spread across a range of customers or are you heavily exposed to a particular customer or vulnerable industry sector?

Inventory

Most of the time, banks or lenders like inventory as it is presumed to be sellable and can be turned into cash. So for them to understand this, they may want to examine your stock turn days (how many days it takes to sell your stock) and your stock age. Banks typically prefer raw or finished inventory since it’s the most marketable in case of default.

Like AR loans, inventory loans move down and up as levels change. Do not expect a lender to grant you a loan that exceeds 50 percent of your inventory-to-loan ratio.

Equipment

In an emergency, owned equipment in good condition can secure a fixed-term loan for a single shot of cash. It’s technically not a short-term loan, and it’s important to remember that the more specialized the equipment is, then the lower loan-to-value will be.

For instance, a 2016 Ford Ute is likely to have a higher value than a 2016 customized trailer.

If you have an excess or old asset that looks marketable, best to sell it for cash. Having extra cash is more valuable than idle equipment.

Factoring

Some SMEs find it better to sell their AR to a third party instead of borrowing on them. This process is called factoring and includes specific terms negotiated between the business and the third party or “factor”.

This includes the ratio of value paid for each invoice, as well as any possible fees to establish and maintain the relationship between the business and factor.Factoring is advantageous particularly if the business is newly established or has damaged credit.

However, personally, I recommend factoring as an extreme, last resort measure.

3. Keep Your Cash Working

Another sensible idea is to keep cash balances in interest-earning accounts. These are available in most banks and in some cases, there is a minimum balance requirement.

If you are routinely struggling with your payables in your business, and you have just now read that you should have spare money sitting in an interest-bearing account, you may be tempted to think I have gone nuts. But that is not the case. Cash shortages affect every business, it is just the frequency that varies.

Setting up your longer-term financial structure will entail identifying what your Capital Reserve should be. We will cover this aspect off in a future article.

It’s best to keep the bulk of your cash in higher-paying accounts. Examples of higher-paying accounts are money market, savings and certificate of deposit (CD).

However, Long-term CD accounts should be avoided, since it locks you in for a certain period of time. Redeeming it early will cost you interest in most cases.

Either invest the portion of your funds which you will not need during the entire life of the CD or go with a penalty-free one.

Final Thoughts

“Cash is king”– is one of the first principles an SME owner usually learns in the early stages of their business.

With the tips I have given above, find the ones that make the most sense for your business.

Remember that working capital is the fuel that runs the business. To provide maximum flexibility and opportunity to your business, you must build and keep a stockpile of cash.

By understanding the options available, you will be better equipped to manage your cash. And, in turn, maintain and grow your operations.

Need help in managing your cash flow? Let Sean help you!

Sean Foster

PS: Interested in working with me? I help in 3 ways:

[1] Work with me privately to improve your business profitability, scale your business & improve your personal and business productivity - Schedule an appointment here.

[2] Join BIG – in-person, group based coaching program. Operating from Silverdale, Auckland

[3] Understand & develop your behavioural habits through psychometric behavioural assessments & coaching

Liking this? Share in your socials: